The idea of receiving $8,000 every month from an investment portfolio without selling a single share sounds almost too good to be true.

For many people pursuing financial freedom, this represents the ultimate destination: building a large portfolio, living from the income it produces and preserving the underlying assets for the future.

Instead of waking up for work because bills need to be paid, your investments would generate enough cash to cover your lifestyle. Instead of worrying about whether you have sold too many shares during a market downturn, distributions would arrive in your account throughout the year.

A recent investment strategy presented by retired investor Brad explored how a $1 million portfolio could potentially generate more than $96,000 in annual distributions. That is the equivalent of $8,000 a month before taxes, fees, currency movements and other costs.

The strategy did not include Bitcoin, gold or other precious metals. It was built primarily around US-listed exchange-traded funds, commonly known as ETFs, that use dividends, preferred securities, energy infrastructure investments and options strategies to generate income.

The proposed portfolio also included something that is often missing from high-income investment plans: a full year of spending held in a separate cash reserve.

The result was not simply a collection of the highest-yielding investments available. The portfolio attempted to combine several different sources of income, including short-term US Treasury bills, energy infrastructure, large US companies, technology companies, small companies and preferred shares.

However, a headline such as “$8,000 a month without selling shares” needs to be examined carefully.

A distribution rate is not the same as a guaranteed return. A fund can pay a high distribution while its share price falls. Some of the money distributed by options-based ETFs may be classified as return of capital. Selling covered calls can also restrict how much an investor benefits when markets rise sharply.

The strategy is therefore better understood as an educational example of how an income-focused portfolio might be constructed, rather than a formula that can be followed blindly.

It also raises a deeper question.

Is the goal of financial freedom simply to receive the highest possible income today, or should we build a portfolio that can continue supporting us for several decades?

That distinction matters because a portfolio that produces impressive distributions for two years is not necessarily the same as one that can protect purchasing power, survive recessions and support a family throughout retirement.

The Powerful Appeal Of Receiving $8,000 A Month Without Selling Shares

Traditional retirement planning often assumes that investors will gradually sell part of their portfolios to pay their living expenses.

Under a withdrawal-based approach, someone with $1 million might withdraw a percentage each year. The remaining money stays invested, and the investor hopes that long-term growth will replace at least some of what has been withdrawn.

There is nothing automatically wrong with selling shares. A total-return investment strategy treats dividends, interest, capital growth and planned asset sales as different parts of the same financial system.

Nevertheless, many people feel uncomfortable selling investments.

When markets are rising, selling a few shares may not feel particularly painful. When markets fall by 20%, 30% or more, the experience becomes emotionally different. Selling during a decline can feel as though years of savings are being permanently destroyed.

This is why an income portfolio can be psychologically attractive.

If dividends and fund distributions cover your expenses, you may feel less pressure to sell investments when prices are depressed. The number of shares in your account can remain unchanged even while cash is regularly transferred into your bank account.

There is also something satisfying about owning an asset that pays you.

A rental property produces rent. A business produces profit. A bond produces interest. A dividend-paying company distributes part of its earnings. An options-based ETF can produce cash by collecting option premiums.

These visible payments can make financial freedom feel real.

However, it is important to understand what “not selling shares” actually means.

Keeping the same number of shares does not guarantee that the value of your capital is being preserved. A fund could distribute 12% during the year while its net asset value falls by 15%. You would still own the same number of shares, but those shares would be worth less.

A distribution may also contain different economic components. It could include company dividends, bond interest, realised investment gains, option premiums or return of capital.

Return of capital is especially misunderstood.

It does not automatically mean that a fund is failing or simply handing investors their own money back. In some options-based funds, return-of-capital treatment can result from the timing and tax classification of option transactions. However, persistent distributions that are not supported by total returns can gradually reduce the value of a portfolio.

This is why investors must examine total return rather than looking only at the amount deposited into their accounts.

Total return includes both:

- the distributions received; and

- the change in the value of the investment.

A portfolio that pays $100,000 but falls in value by $150,000 has not made the investor $100,000 richer. Economically, the investor has experienced a $50,000 loss before taxes and costs.

The goal should therefore not be to chase the largest visible yield. The goal should be to create a sustainable relationship between income, growth and risk.

The $8,000-a-month strategy attempts to do this by spreading the portfolio across several income-producing funds rather than placing the entire $1 million into one exceptionally high-yielding ETF.

It also deliberately includes different fund providers. This can reduce dependence on one investment company, one portfolio management team or one specific options process.

Yet issuer diversification should not be confused with complete investment diversification.

Several funds in the proposed portfolio still depend on US equity markets and options premiums. During a severe market decline, correlations can increase and apparently different investments may fall together.

The income target is therefore possible only because the portfolio accepts meaningful market risk.

Generating $96,000 from $1 million requires a portfolio-level cash distribution of approximately 9.6% a year. That is considerably higher than the income normally associated with cash deposits, government bonds or a conventional portfolio of dividend-paying companies.

The additional income does not appear from nowhere.

It comes from accepting risks such as equity-market exposure, options exposure, energy-sector concentration, small-company volatility, interest-rate sensitivity, credit risk and the possibility that future distributions will be reduced.

The strategy can still be useful, but the $8,000 headline should be viewed as an income target rather than a promise.

Why A $96,000 Cash Reserve Comes Before The Investment Portfolio

One of the most sensible parts of the strategy is the decision to separate one year of planned spending before investing the rest of the money.

If the desired income is $8,000 a month, one year of spending equals:

$8,000 × 12 = $96,000

The original $1 million is therefore divided into two broad sections:

| Portfolio section | Amount |

|---|---|

| One-year cash reserve | $96,000 |

| Income-producing investments | $904,000 |

| Total | $1,000,000 |

This cash reserve is designed to reduce sequence-of-returns risk.

Sequence risk refers to the danger of experiencing poor investment returns near the beginning of retirement or during the first years of drawing income.

Imagine two retired investors who receive exactly the same average return over 20 years. One experiences strong returns at the beginning and market declines later. The other suffers a major crash during the first two years and receives stronger returns afterwards.

Even if their long-term average returns are identical, the second investor may end up with considerably less money if substantial withdrawals were made while the portfolio was depressed.

The order in which returns occur matters when money is being withdrawn.

A cash reserve provides a temporary buffer. If markets fall, the investor can use the reserve to pay living expenses rather than immediately selling investments or relying entirely on distributions that may be reduced.

In the proposed strategy, the reserve is not necessarily left in a non-interest-paying current account. It is divided between SGOV and CSHI.

SGOV is the iShares 0–3 Month Treasury Bond ETF. It invests in very short-term US Treasury securities. As of 9 July 2026, its reported 30-day SEC yield was 3.57%, its 12-month trailing yield was 3.80%, and its expense ratio was 0.09%.

Because the underlying Treasury securities have very short maturities, SGOV generally has much less interest-rate sensitivity than a conventional long-term bond fund.

That does not make it identical to money held in an insured bank account. SGOV is still an exchange-traded investment, and its market price can fluctuate. Nevertheless, it is intended to provide highly liquid exposure to short-dated US government debt.

CSHI is the NEOS Enhanced Income 1–3 Month T-Bill ETF. It combines a portfolio of short-term Treasury bills with a put-option strategy designed to produce additional monthly income. NEOS reported a distribution rate of 4.69% and a 30-day SEC yield of 3.23% in its June 2026 fund information.

CSHI may produce more income than a straightforward Treasury-bill fund, but it also introduces options-related risk. It should not automatically be treated as equivalent to cash.

That is an important distinction.

An emergency reserve normally exists to provide certainty, accessibility and protection. The more investment risk added to the reserve, the less dependable it may become during the exact period in which it is needed.

A cautious investor might therefore choose to hold some money in an actual bank or money-market account and place only part of the reserve into short-term Treasury ETFs.

The correct structure depends on spending requirements, taxes, account access and personal tolerance for volatility.

The deeper lesson is that financial freedom requires liquidity.

People often concentrate entirely on their net worth. They may own investments, property, pensions and business assets while having very little immediately available cash.

A person can be wealthy on paper and still experience financial pressure if monthly bills cannot be paid without selling something.

A well-designed cash bucket provides time.

It gives markets time to recover.

It gives an investor time to review falling distributions.

It provides money for emergencies that have nothing to do with the stock market.

It can also reduce emotional decision-making. An investor who knows that the next twelve months of expenses have already been covered may be less likely to panic during a sharp correction.

The downside is that holding $96,000 in a lower-returning reserve creates an opportunity cost. That money could potentially earn more if invested in equities.

However, maximising returns is not the only purpose of a retirement portfolio.

The portfolio must also help its owner sleep at night.

A reserve that prevents one disastrous, fear-driven decision may be worth far more than the additional return that could have been earned by investing every available dollar.

The Six Income ETFs Used To Build The Main Portfolio

After setting aside the $96,000 reserve, approximately $904,000 remains available for the main income portfolio.

The proposed strategy divides this money equally between six ETFs. An equal allocation would place approximately $150,667 into each fund.

The six funds are MLPI, OVL, EDGX, TDAQ, GPIQ and PFFA.

Each fund attempts to generate income in a different way, although several use options as part of their strategies.

MLPI: energy infrastructure and options income

MLPI is the NEOS MLP & Energy Infrastructure High Income ETF.

The fund invests in master limited partnerships and energy infrastructure businesses while also using call options to generate monthly income. NEOS states that the fund aims to combine high monthly income with the potential for capital appreciation. It also provides Form 1099 reporting in the United States rather than the more complicated K-1 reporting normally associated with directly owned master limited partnerships.

As of June 2026, NEOS reported a distribution rate of approximately 14.48% for MLPI.

This is a high level of income, but it comes with concentrated exposure to the energy infrastructure sector. Energy demand, commodity prices, interest rates, regulation and the financial strength of individual operators can all influence returns.

MLPI also had a relatively short operating history, having launched in December 2025. Strong early performance cannot tell investors how the fund will behave throughout a full economic or commodity cycle.

OVL: large US companies with a put-spread overlay

OVL is the Overlay Shares Large Cap Equity ETF.

The fund owns large-capitalisation US equity exposure and uses a put-spread strategy to seek additional income. The strategy generally involves selling short-term put options and buying lower-strike put options to limit part of the downside obligation.

As of 10 July 2026, OVL reported a monthly distribution rate of 10.28% and a 30-day SEC yield of 1.00%.

The difference between those two figures is worth noticing.

The 30-day SEC yield is a standardised measure primarily reflecting the income generated by the underlying investments after expenses. The much higher distribution rate annualises the most recent payment and can include income generated by the options strategy.

OVL’s prospectus warns that options can produce losses when the underlying market moves adversely. It also explains that options use may reduce the fund’s ability to benefit fully from rising markets.

The fund may therefore produce useful income in certain market conditions, but it should not be assumed to outperform the S&P 500 continuously.

EDGX: weekly income from large US companies

EDGX is the Global X U.S. 500 Income Edge ETF.

The fund seeks exposure to approximately 500 large US-listed companies while selling call options on part of the portfolio.

Global X targets a 9% annualised distribution rate and intends to pay distributions weekly. The fund normally writes calls against only part of its assets so that it can retain some participation when the equity market rises.

Weekly distributions may appeal to investors who like frequent cash flow. However, payment frequency does not by itself improve an investment’s return.

Receiving $100 once a month and receiving approximately $23 a week are economically similar if the annual total is the same.

EDGX was launched in February 2026, giving it a very limited performance record. Its net assets were approximately $4.82 million as of 10 July 2026, although its net expense ratio was temporarily reduced to zero under a fee waiver scheduled to remain in effect until at least March 2027.

A new fund may perform well, but investors should be careful about drawing long-term conclusions from a few months of market data.

TDAQ: Nasdaq-100 exposure with daily options

The transcript refers to this fund as “TDAC”, but the correct ticker is TDAQ.

TDAQ is the TappAlpha Innovation 100 Growth & Daily Income ETF. It seeks current income while maintaining potential for capital appreciation and exposure to the Nasdaq-100 Index.

TappAlpha uses a daily covered-call approach. Instead of selling options only once a month, the strategy can sell short-dated, out-of-the-money options on a daily basis. This is intended to capture recurring option premiums while allowing the managers to adjust the strategy as conditions change.

The fund reported a distribution rate of approximately 16.98% around the time reflected in the original strategy. Its official disclosures explain that the distribution rate annualises the most recent payment and is not a measure of total return. The fund also warns that distributions can exceed its income and realised gains, with the excess treated as return of capital.

TDAQ provides exposure to some of the largest technology and growth-oriented companies in the United States. That creates significant growth potential, but it can also create concentration risk.

The Nasdaq-100 can experience sharp price movements. Selling calls may provide premium income and some limited cushioning, but it cannot eliminate losses during a serious technology-sector decline.

GPIQ: a more established Nasdaq income strategy

GPIQ is the Goldman Sachs Nasdaq-100 Premium Income ETF.

Like TDAQ, it seeks to combine Nasdaq-100 exposure with options-generated income. Goldman Sachs typically sells calls against part of the portfolio rather than covering every holding completely.

The prospectus states that the normal overwrite level is expected to range between 25% and 75% of the equity portfolio. This provides the managers with flexibility to balance current income against potential market appreciation.

GPIQ’s 12-month trailing distribution rate was 9.33% as of 30 June 2026.

The fund’s distributions can include substantial return-of-capital classifications. Goldman Sachs reported that approximately 88.3% of GPIQ’s distributions had been classified as return of capital as of 31 March 2026, although that percentage can change and does not by itself prove that the fund is destroying capital.

The more important question is whether the fund’s total return and net asset value can support the payments over time.

PFFA: preferred securities and monthly income

PFFA is the Virtus InfraCap U.S. Preferred Stock ETF.

Preferred securities sit between ordinary shares and corporate debt. They generally have priority over common shares when dividends are paid, but they remain below bonds and other senior debt in a company’s capital structure.

PFFA seeks current income and, secondarily, capital appreciation through a portfolio of preferred securities issued by US companies.

As of 9 July 2026, the fund reported a distribution rate of 9.91% and a 30-day SEC yield of 9.71%.

The fund declared a monthly distribution of $0.1725 per share at the beginning of 2026, equivalent to $2.07 a share on an annualised basis, although future payments are planned rather than guaranteed.

PFFA is intended to bring a different source of income into the portfolio. However, preferred securities can be sensitive to interest rates, credit conditions and financial-sector stress. PFFA also uses leverage, which can increase both income and losses.

The fund should therefore not be treated as a risk-free substitute for cash or government bonds.

How The Portfolio Could Produce More Than $96,000 A Year

Using equal allocations and the distribution rates available around June and July 2026, it is possible to estimate the portfolio’s potential annual cash flow.

The figures below are illustrative. Distribution rates change, payments can be reduced and actual income will depend on purchase prices, ex-dividend dates, taxes and future fund decisions.

| Fund | Approximate allocation | Illustrative distribution rate | Estimated annual distributions |

| MLPI | $150,667 | 14.48% | $21,818 |

| OVL | $150,667 | 10.28% | $15,491 |

| EDGX | $150,667 | 9.00% target | $13,560 |

| TDAQ | $150,667 | 16.98% | $25,586 |

| GPIQ | $150,667 | 9.33% | $14,058 |

| PFFA | $150,667 | 9.91% | $14,932 |

| Main portfolio | $904,000 | Approximately $105,445 |

The main portfolio could therefore produce approximately $105,445 in annual distributions if all the quoted distribution rates remained unchanged.

That is approximately:

$105,445 ÷ 12 = $8,787 per month

The cash bucket may also produce income.

For example, suppose the $96,000 reserve were divided equally:

- $48,000 in SGOV at an illustrative 3.80% trailing yield; and

- $48,000 in CSHI at an illustrative 4.69% distribution rate.

The estimated annual cash flow would be:

| Cash holding | Allocation | Illustrative rate | Estimated annual income |

| SGOV | $48,000 | 3.80% | $1,824 |

| CSHI | $48,000 | 4.69% | $2,251 |

| Cash reserve total | $96,000 | Approximately $4,075 |

When the two sections are combined, the total estimated distributions become:

$105,445 + $4,075 = $109,520 a year

That is approximately:

$109,520 ÷ 12 = $9,127 a month

On paper, the portfolio exceeds the original $8,000 monthly target by more than $1,100.

This surplus could serve several purposes.

Part of it could be reinvested to purchase additional shares. Reinvestment might help the portfolio keep pace with inflation and replace capital lost through unfavourable market movements.

Part of it could remain in the reserve. If the investor spent $96,000 but received approximately $109,520, the theoretical surplus would be around $13,520 before tax.

The surplus could also offset months in which distributions fall.

However, these calculations contain several assumptions.

They assume that every quoted distribution continues at the same level.

They assume that the investor can purchase the funds at prices similar to those used when the distribution rates were calculated.

They ignore brokerage costs, bid-and-offer spreads, foreign-exchange charges and taxes.

They also assume that the funds preserve enough capital for the strategy to remain viable.

A distribution rate is usually calculated by annualising a recent payment. If a fund pays 1% of its net asset value during one month, the published distribution rate might be shown as approximately 12%.

That does not mean the fund has contractually promised to pay 12% during the next year.

It means that the latest payment would equal approximately 12% if repeated for twelve months and measured against the relevant net asset value.

Fund providers themselves warn investors not to interpret distribution rates as total returns. NEOS, TappAlpha and Global X all explain that an annualised distribution rate is based on a recent payment and should not be treated as a representation of the fund’s total performance.

This is why a responsible investor would not immediately spend every dollar received.

A more conservative approach might involve spending only $8,000 of the estimated $9,127 monthly cash flow and retaining the difference.

Even then, the portfolio would need regular monitoring.

If the total value declined for several consecutive years, the investor might reduce withdrawals, rebalance the portfolio or replace funds that no longer supported the original objectives.

Financial freedom does not remove the need for financial management.

It simply changes the nature of the work.

Instead of working exclusively for wages, the investor must manage assets, spending, taxes and risk.

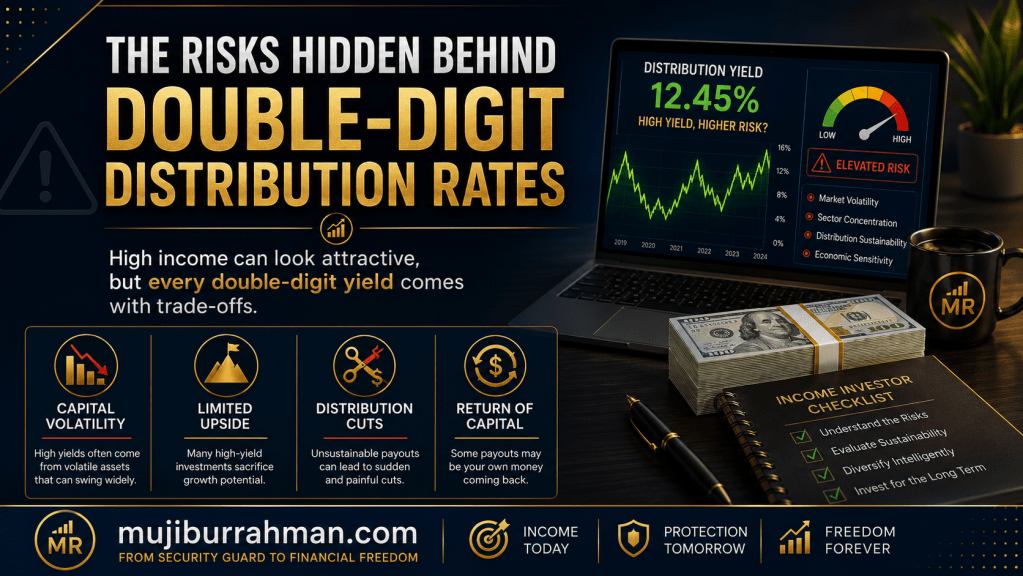

The Risks Hidden Behind Double-Digit Distribution Rates

High income is attractive because it appears to solve the central problem of retirement: how to replace employment earnings.

But high distributions are normally accompanied by significant risks.

The first is capital volatility.

Most of the proposed portfolio is not held in cash or conventional bonds. It is connected to equities, preferred securities, energy infrastructure and options markets.

If the S&P 500 or Nasdaq-100 falls sharply, funds such as OVL, EDGX, TDAQ and GPIQ can also decline. Option premiums may provide some income, but they are not guaranteed to offset major losses.

Goldman Sachs explicitly warns that option premiums may not fully protect GPIQ during market declines and that the fund could experience sharp falls in net asset value during a severe equity-market sell-off.

The second risk is limited upside.

Covered-call strategies generate income by selling someone else the right to benefit from part of a market increase.

The premium received is real income, but the trade-off is that gains can be restricted when the underlying market rises strongly.

This does not mean covered-call ETFs always underperform. Outcomes depend on the percentage of the portfolio covered, the strike prices chosen, market volatility and the manager’s execution.

Nevertheless, investors should understand that high current income may be created partly by giving away future upside.

The third risk is distribution reduction.

None of these funds guarantees its current payment.

Option premiums tend to be influenced by market volatility. Dividends can be cut. Interest rates can fall. Preferred issuers can suspend payments. Fund managers can change distribution policies.

A portfolio producing $109,000 today may not produce the same amount next year.

A financial plan that requires every dollar of the current distribution leaves very little room for disappointment.

The fourth risk is return of capital.

Return of capital can sometimes be tax-efficient and does not automatically mean an investment is failing.

However, investors must determine whether distributions are supported by economic returns.

Suppose a fund begins the year at $25, distributes $3 and ends at $20.

The investor received 12% of the original share price in cash, but the share price declined by 20%. The total return was negative before considering reinvestment or taxes.

Receiving a distribution does not cancel the decline in value.

The fifth risk is concentration.

MLPI concentrates on energy infrastructure.

TDAQ and GPIQ focus heavily on the Nasdaq-100.

EDGX and OVL depend on large US companies.

IWMI, included as a bonus holding, focuses on smaller US businesses.

PFFA concentrates on preferred securities and can have meaningful exposure to financial, utility and infrastructure issuers.

The overall portfolio is broader than a single ETF, but it remains heavily exposed to the United States.

It has little direct allocation to developed markets outside America, emerging markets, conventional investment-grade bonds or property.

The sixth risk is fund age.

Several of the ETFs are relatively new.

EDGX began trading in February 2026.

MLPI launched in December 2025.

TDAQ also has a short operating record compared with long-established index funds.

New strategies can work extremely well, but they have not yet been tested through many different market environments.

A fund that performs well during a strong or rising market may behave differently during a recession, credit crisis or prolonged bear market.

The seventh risk is inflation.

Receiving $8,000 a month may feel comfortable today, but its purchasing power could decline significantly over a long retirement.

If spending rises by 3% a year, a lifestyle costing $96,000 today would cost approximately $129,000 after ten years.

The portfolio must therefore preserve some capacity for growth.

Spending every distribution may produce a generous income today while leaving too little capital to support tomorrow’s higher expenses.

The eighth risk is taxation and accessibility, particularly for British investors.

These are US-listed ETFs. Some UK retail platforms may not make certain US ETFs available when the required retail disclosure documents are not provided. UK rules require appropriate product disclosures before relevant packaged investments are marketed to retail clients.

A UK investor may also face US withholding tax on certain US-source distributions. A reduced treaty rate may be available when the appropriate requirements are met and a valid W-8BEN form is held by the broker.

Foreign income may also need to be reported to HMRC, depending on the amount and the investor’s wider circumstances. Gains from offshore funds can receive different UK tax treatment depending on whether a fund has UK reporting-fund status.

This means a British investor should not assume that a 10% published US distribution rate becomes a 10% spendable return in pounds.

Currency movements between the pound and the dollar can increase or reduce the value of both income and capital.

Tax treatment can also be complex, particularly when distributions contain dividends, option-related income or return of capital under US classifications.

The strategy should therefore be discussed with a properly qualified financial adviser or tax professional before real money is committed.

The Two Bonus Ideas That Could Strengthen The Portfolio

The original presentation included two additional ideas.

The first was adding IWMI to provide exposure to smaller US companies.

IWMI is the NEOS Russell 2000 High Income ETF. It seeks monthly income and potential capital appreciation by combining Russell 2000 exposure with call options.

As of 30 June 2026, NEOS reported a distribution rate of 14.42%, a 12-month trailing distribution rate of 13.59% and a 30-day SEC yield of 0.50%.

The large difference between the SEC yield and distribution rate again indicates how important the options component is to the fund’s cash payments.

IWMI could improve diversification because small companies do not always move in the same way as the largest technology and multinational businesses.

Smaller companies may benefit more directly from domestic economic growth, improving credit conditions or falling interest rates.

However, small-company shares also tend to be more volatile. They may have weaker balance sheets, less access to capital, narrower profit margins and a greater risk of business failure than established large companies.

The addition of IWMI therefore provides a different type of equity exposure, not a low-risk asset.

If the $904,000 were divided equally between seven income funds instead of six, each position would receive approximately $129,143.

Using the same illustrative rates, the average portfolio distribution could remain close to 12%, although the exact outcome would change whenever the funds adjusted their payments.

The advantage would be broader exposure across:

- large US companies;

- Nasdaq growth companies;

- smaller US companies;

- energy infrastructure;

- preferred securities; and

- several options-income processes.

The disadvantage would be increased complexity.

Every additional fund creates more information to monitor. Investors must track distributions, net asset values, options strategies, expenses, tax documents and changes made by the provider.

Diversification is valuable, but collecting funds without understanding them can create the illusion of safety.

The second bonus idea was beginning with approximately $1.096 million instead of $1 million.

Under this version, the entire $1 million would be invested in the income-producing ETFs, while the separate $96,000 reserve would sit outside the investment allocation.

The structure would therefore be:

| Portfolio section | Amount |

| Main income portfolio | $1,000,000 |

| Separate one-year reserve | $96,000 |

| Total starting capital | $1,096,000 |

At an average distribution rate of approximately 12%, the $1 million investment portfolio could generate around $120,000 annually.

That equals:

$120,000 ÷ 12 = $10,000 a month

An investor spending $8,000 a month would have an estimated $2,000 monthly margin before taxes and costs.

This creates approximately 1.25 times the required income:

$120,000 ÷ $96,000 = 1.25

The original presentation described the goal as being close to 1.3 times the required annual spending.

This additional coverage is valuable because it creates flexibility.

If distributions fall by 15%, the investor may still receive enough to cover the planned lifestyle.

If inflation increases expenses, some of the surplus may absorb the rise.

If the funds perform well, the unused income can be reinvested.

Starting with additional capital also means the reserve does not reduce the size of the income-producing portfolio.

This highlights one of the most powerful truths about passive income: capital matters.

A person with $1 million does not need to take the same risks as someone attempting to generate $8,000 a month from $300,000.

To produce $96,000 from $300,000 would require a 32% annual distribution. That would be extremely difficult to sustain and would expose the investor to exceptional risk.

To produce the same income from $2 million requires only 4.8%.

The larger the capital base, the less yield is needed.

This is why the accumulation stage of financial freedom is so important.

People sometimes spend years searching for a magical high-yield investment when the more dependable solution is to increase savings, earnings, business income and invested capital.

A bigger portfolio creates more choices.

It allows the investor to use lower-risk assets, hold more cash, diversify internationally and survive reductions in income.

The most sustainable income strategy may therefore begin long before retirement. It begins with building the largest realistic base of productive assets.

What This Strategy Teaches Me About My Journey From Security Guard To Financial Freedom

I am not currently sitting on a $1 million investment portfolio.

I still work long hours as a security guard, including demanding night shifts, while building my blogs, researching online businesses and working towards financial freedom.

It would be easy for me to look at a million-dollar portfolio and feel that the subject has no relevance to my present life.

But every large portfolio begins somewhere.

It begins with the first amount saved instead of spent.

It grows through regular investing.

It grows when someone develops a new skill, earns additional income or creates a digital asset.

It grows when profits are reinvested rather than immediately absorbed by lifestyle inflation.

The most important lesson from this strategy is not the names of the six ETFs.

Fund names will change.

Distribution rates will rise and fall.

New products will be launched, and some existing funds may eventually close.

The enduring lesson is that financial freedom requires assets capable of producing cash flow.

For most of my working life, my income has depended on my presence.

I travel to work.

I complete a shift.

I exchange a specific number of hours for a specific amount of money.

When the shift ends, the payment ends.

An investment portfolio works differently.

The capital continues working whether its owner is awake or asleep. Dividends, interest and option premiums do not require the investor to stand at a security desk for twelve hours.

That is the type of freedom I am working towards.

However, I also understand that reaching it will require patience.

A $1 million portfolio is not normally built through one dramatic decision. It is built through thousands of smaller decisions repeated over many years.

It may begin with investing £10.

Then £100.

Then £500.

The amount matters, but the identity being developed matters too.

Every investment is evidence that I am becoming an owner rather than remaining only a worker.

My employment income pays today’s expenses. My assets are being built to pay tomorrow’s expenses.

The second lesson is that income alone is not enough.

When I first became interested in passive income, it was tempting to focus entirely on the largest percentage available.

A 15% distribution looks better than a 5% yield.

But a high number does not tell the complete story.

I must ask where the income comes from.

I must understand what happens to the capital.

I must look at expenses, diversification, risk, taxes and total return.

I must consider how the investment might behave when markets fall rather than looking only at what it did during good times.

This applies beyond the stock market.

A blog can produce advertising revenue, but only if it continues attracting readers.

An ebook can generate sales, but only if it provides value and remains visible.

An affiliate website can earn commission, but only while people trust its recommendations and the affiliate programme continues operating.

Every income stream has risks.

Financial freedom is not created by pretending those risks do not exist. It is created by understanding them and avoiding dependence on one fragile source.

The third lesson is the importance of a cash reserve.

For someone working towards freedom, cash may not appear exciting. Investing every spare pound seems more productive.

But a reserve protects the journey.

Without emergency savings, an unexpected bill can force me to sell investments, use expensive debt or abandon a business project.

Cash provides breathing space.

It allows me to continue investing during difficult periods.

It reduces the chance that one financial emergency will destroy years of progress.

The fourth lesson is that I need a margin of safety.

If my future lifestyle requires £3,000 a month, I should not build a plan that produces exactly £3,000 under perfect conditions.

I should aim for more.

Some months will be weaker.

Advertising income will fluctuate.

Markets will fall.

Expenses will rise.

Businesses will change their terms.

A target of £4,000 or £5,000 could provide greater protection than depending on the minimum amount required to survive.

The same principle appears in the $1.096 million bonus portfolio. Producing $120,000 when only $96,000 is needed creates room for reinvestment, inflation and disappointing periods.

The fifth lesson is that I do not need to wait until I am wealthy to practise wealth-building behaviour.

I can create my own small version of the portfolio today.

I may not receive $8,000 a month, but I can begin building assets that produce £8, then £80, then £800.

The first milestone is not financial freedom.

The first milestone is proving that money can arrive from an asset rather than from another hour of employment.

That first dividend payment matters.

The first affiliate commission matters.

The first ebook sale matters.

The first day of advertising income matters.

Each payment demonstrates that the relationship between time and money can be changed.

My long-term goal is not simply to leave my job.

It is to build a life in which work becomes a choice rather than an obligation.

That requires more than one high-yield portfolio.

It requires investment capital, online income, useful skills, discipline and the willingness to continue learning.

The $8,000-a-month portfolio provides an interesting picture of what the destination could look like. A collection of assets produces enough income to support its owner, while a separate reserve provides security during difficult markets.

But the destination will never be reached by staring at the final number.

It will be reached by concentrating on the next step.

For me, that means continuing to write.

It means publishing useful articles.

It means improving my websites.

It means building digital products and investing part of what I earn.

It means using my remaining working years not only to pay bills, but to accumulate assets that can eventually replace my wages.

I do not know whether my future income portfolio will contain MLPI, OVL, EDGX, TDAQ, GPIQ, PFFA or completely different funds.

What I do know is that I want to own productive assets.

I want my money to work alongside me.

Then, eventually, I want those assets to work hard enough that I no longer have to exchange most of my waking life for a wage.

That is the real promise behind the idea of earning $8,000 a month without selling shares.

It is not simply a portfolio calculation.

It is a vision of independence.

It is the point at which years of saving, learning, investing and building finally create control over time.

That is why I continue this journey.

Not because financial freedom will be easy, and not because any investment can guarantee it.

I continue because every asset I build moves me a little closer to a life based on choice rather than necessity.

From Security Guard To Financial Freedom.

Disclaimer

The information provided in this article is for educational and informational purposes only. It is not intended to be financial, investment, legal, tax, or professional advice. The views and strategies discussed are based on general wealth-building principles and personal finance concepts and may not be suitable for every individual situation.

Before making any financial decisions, including investing, saving, borrowing, or changing your financial strategy, you should conduct your own research and consult with a qualified financial adviser, accountant, or other professional who can assess your specific circumstances.

While every effort has been made to ensure the accuracy of the information presented, no guarantees are made regarding the completeness, reliability, or future performance of any financial strategy, investment, or asset mentioned. All investments carry risk, and past performance is not a guarantee of future results. You may lose some or all of your invested capital.

The author and publisher are not responsible for any financial losses, damages, or consequences resulting from the use of the information contained in this article. Readers are encouraged to make informed decisions and take personal responsibility for their financial choices.